Get Maximum Tax Refund Without Fake Investments: Smart and Legal Ways to Save Tax in 2026

Get Maximum Tax Refund Without Fake Investments: Smart and Legal Ways to Save Tax in 2026

Many taxpayers start searching for tax-saving options only when the financial year is about to end. In a hurry to reduce taxes, some people make unnecessary investments, while others submit incorrect or fake investment proofs. This approach is risky and can lead to penalties, notices, or rejected tax benefits. The good news is that you do not need fake investments to save tax or get a bigger tax refund. With proper tax planning and awareness of available deductions, you can legally reduce your tax liability and maximize your refund. In this guide, we will explain practical and legal ways to save tax in 2026 and claim the maximum refund you deserve.

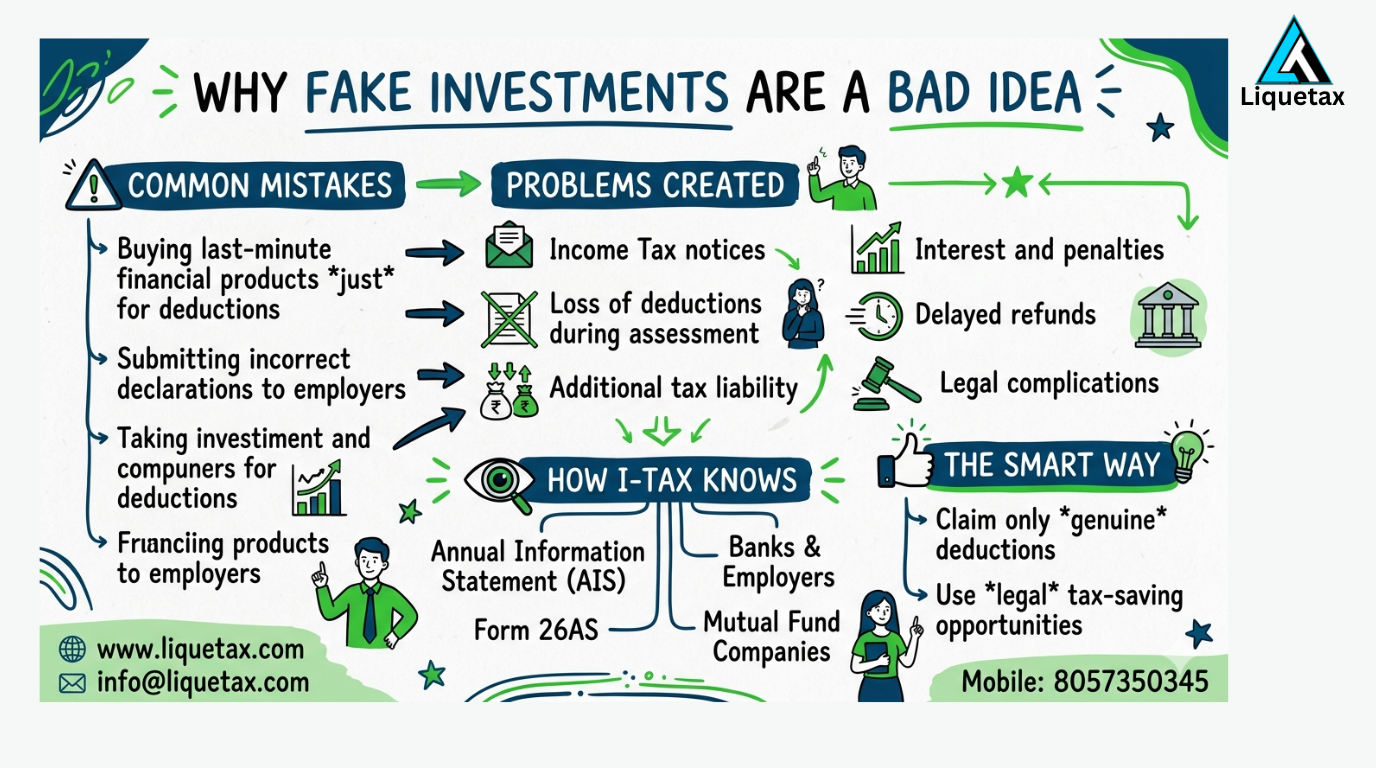

Why Fake Investments Are a Bad Idea

Some taxpayers purchase financial products at the last minute simply to claim deductions. Others may submit incorrect declarations to their employers. This can create several problems: Income Tax notices Loss of deductions during assessment Additional tax liability Interest and penalties Delayed refunds Legal complications The Income Tax Department now has access to extensive financial information through AIS (Annual Information Statement), Form 26AS, banks, employers, mutual fund companies, and other reporting entities. As a result, incorrect claims are easier to identify than ever before. The safest and smartest approach is to claim only genuine deductions and use legal tax-saving opportunities.

Understanding Tax Refunds

A tax refund occurs when the tax paid during the year exceeds your actual tax liability. This can happen because of: Excess TDS deducted by employer TDS deducted on fixed deposits Advance tax paid in excess Tax-saving deductions not considered earlier Tax credits missed during salary processing The goal is not simply to get a refund but to ensure that you pay only the correct amount of tax.

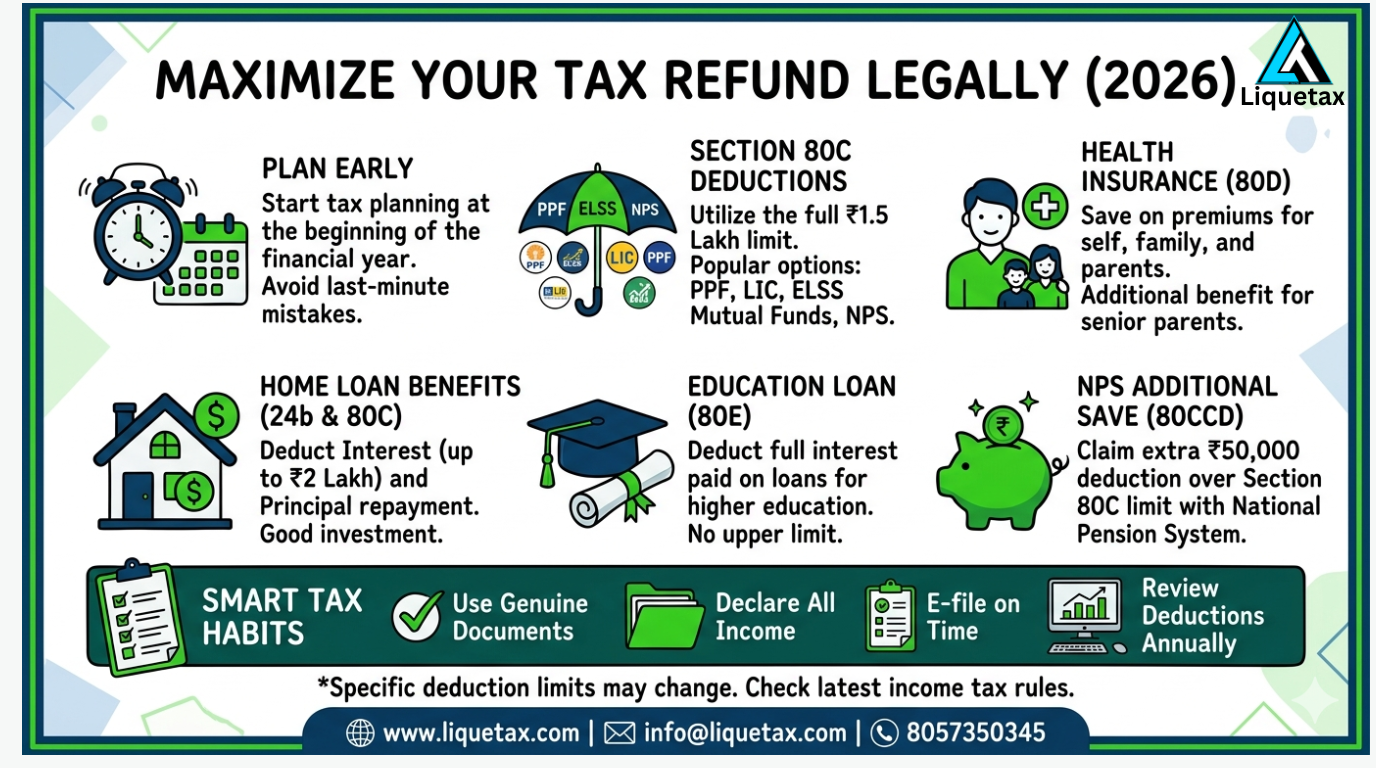

Smart and Legal Ways to Save Tax in 2026

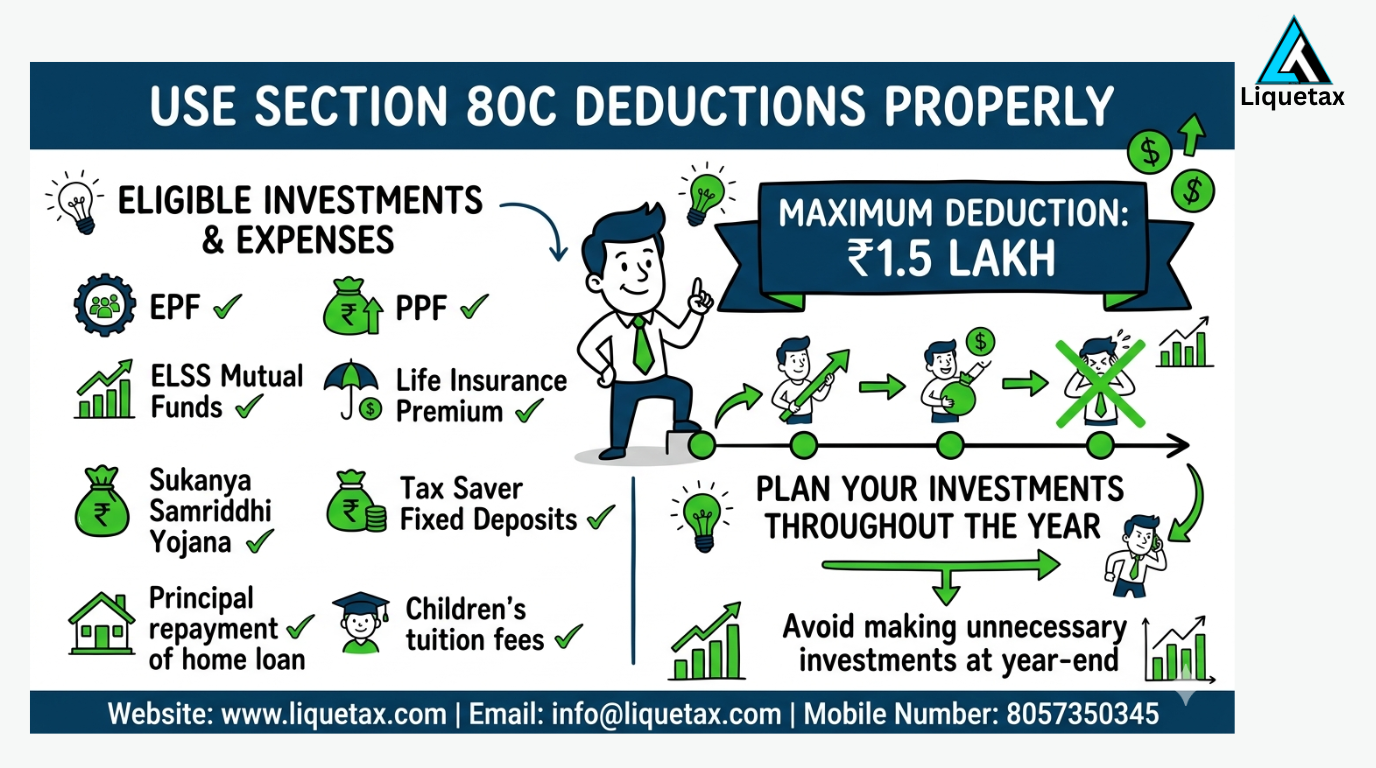

1. Use Section 80C Deductions Properly

Section 80C remains one of the most popular tax-saving provisions under the old tax regime. Eligible investments and expenses include: Employee Provident Fund (EPF) Public Provident Fund (PPF) ELSS Mutual Funds Life Insurance Premium Sukanya Samriddhi Yojana Tax Saver Fixed Deposits Principal repayment of home loan Children's tuition fees The maximum deduction available under Section 80C is ₹1.5 lakh. Instead of making unnecessary investments at year-end, plan your investments throughout the year.

2. Claim Health Insurance Under Section 80D

Health insurance not only protects your family but also provides tax benefits. You can claim deductions for: Self and family health insurance premiums Parents' health insurance premiums Preventive health checkups Many taxpayers forget to claim these deductions, resulting in higher tax liability.

3. Claim Home Loan Benefits

If you have a home loan, significant tax benefits may be available. Under the old tax regime: Principal repayment may qualify under Section 80C. Interest on self-occupied property may qualify up to prescribed limits. These benefits can substantially reduce taxable income.

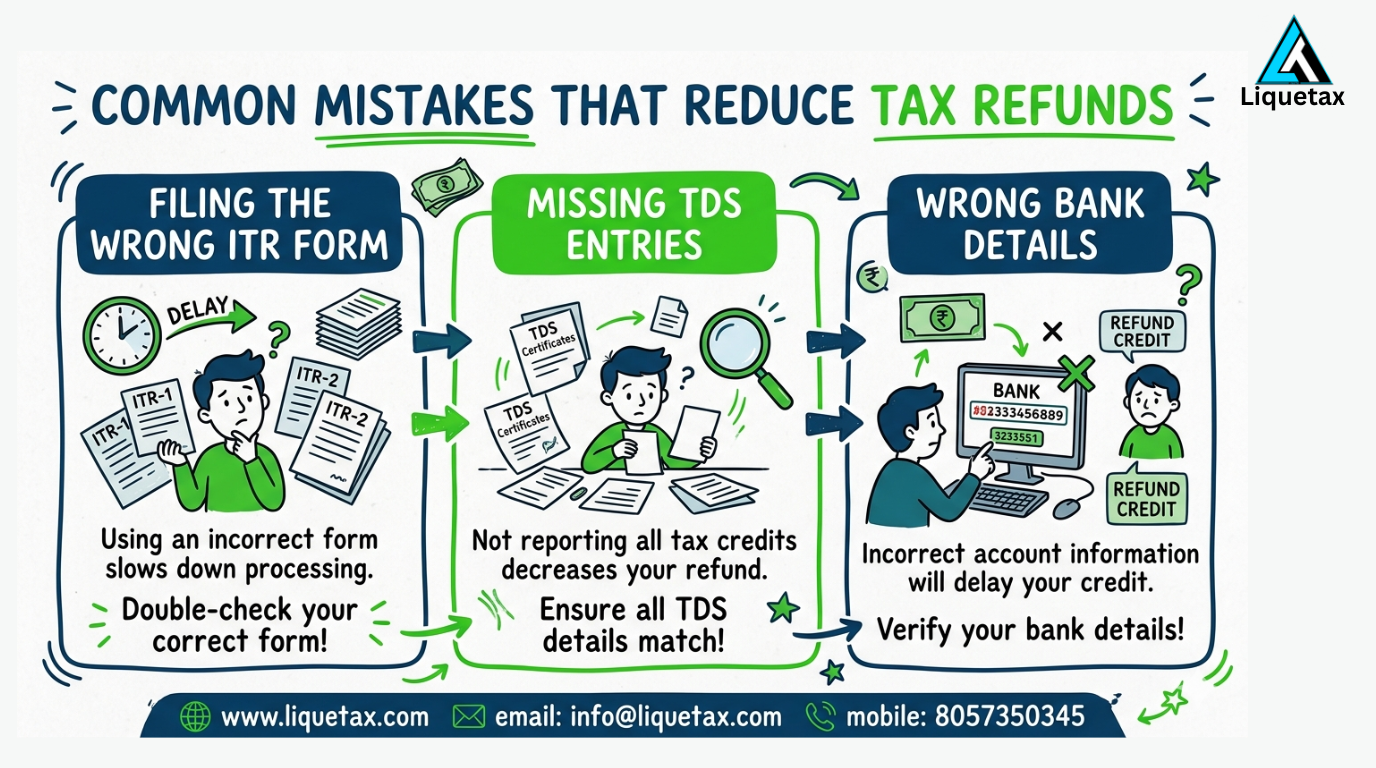

Common Mistakes That Reduce Tax Refunds

Many taxpayers lose part of their refund because of avoidable mistakes. Common examples include:

Filing the Wrong ITR Form

Using an incorrect return form can delay processing.

Missing TDS Entries

Failure to report all TDS credits can reduce refunds.

Wrong Bank Details

Incorrect bank account information may delay refund credit.

Ignoring AIS Information

Mismatch between AIS and ITR may trigger adjustments.

Claiming Ineligible Deductions

Unsupported deductions may be disallowed. Avoiding these mistakes helps ensure faster and accurate refund processing.

Benefits of Legal Tax Planning

Legal tax planning offers several advantages: Higher tax savings Faster refunds Reduced stress Better financial management Compliance with tax laws Lower risk of notices Improved investment decisions The objective should always be long-term financial growth rather than last-minute tax-saving decisions.

How Liquetax Can Help

Tax laws change regularly, and many taxpayers struggle to identify deductions, choose the right tax regime, and file returns accurately. At Liquetax, our experts help individuals, professionals, freelancers, and businesses with: Income Tax Return Filing Tax Planning Refund Assistance TDS Compliance GST Services Business Registration Annual Compliance Services We ensure that you claim all eligible deductions legally and receive the maximum refund available under the law.

Conclusion

You do not need fake investments to save tax or increase your refund. Smart tax planning, proper documentation, accurate reporting, and awareness of available deductions can help you reduce your tax liability legally. Instead of making rushed financial decisions at the end of the year, start planning early and use genuine tax-saving opportunities. This approach not only helps you save money but also protects you from future tax complications. Remember, the best tax-saving strategy is one that is legal, transparent, and aligned with your financial goals.

Contact Liquetax

Need professional help with tax planning or ITR filing? 🌐 Website: www.liquetax.com 📧 Email: info@liquetax.com 📞 Mobile: 8057350345 Get expert guidance and maximize your tax refund the right way with Liquetax.

Frequently Asked Questions (FAQs)

Q1. Can I get a higher tax refund without making new investments?

Yes. By correctly claiming eligible deductions, reporting all tax credits, and filing accurately, you may receive a higher refund.

Q2. Are fake investment proofs risky?

Yes. Fake or incorrect investment claims can lead to notices, penalties, and disallowed deductions.

Q3. Which tax regime is better for maximum refund?

It depends on your income and deductions. Comparing both regimes before filing is important.

Q4. Why should I check Form 26AS before filing my ITR?

Form 26AS shows tax credits available to you. Missing credits can reduce your refund.

Q5. What is AIS and why is it important?

AIS contains details of your financial transactions and helps ensure accurate income reporting.