How Traders & Small Businesses Can Reduce Tax Legally: Complete Tax Saving Guide for FY 2026-27

How Traders & Small Businesses Can Reduce Tax Legally: Complete Tax Saving Guide for FY 2026-27

Introduction

Every trader and small business owner wants to increase profits and reduce unnecessary expenses. One of the biggest expenses for businesses is income tax. The good news is that Indian tax laws provide several legal ways to reduce your tax burden while staying fully compliant. Many traders and small business owners end up paying more tax than required because they are unaware of available deductions, exemptions, and tax-saving strategies. Proper tax planning can help you save thousands or even lakhs of rupees every year. In this comprehensive guide, we will explain the best legal tax-saving methods for traders, shop owners, wholesalers, retailers, manufacturers, consultants, and small business owners for FY 2026-27.

Why Tax Planning Is Important

Tax planning is not about avoiding taxes. It is about using the provisions available under Indian tax laws to reduce your tax liability legally.

'Benefits of Tax Planning

Reduces overall tax burden Improves business cash flow Increases profitability Helps in financial planning Prevents penalties and notices Ensures legal compliance A well-planned business can save a significant amount of money every year through proper tax management.

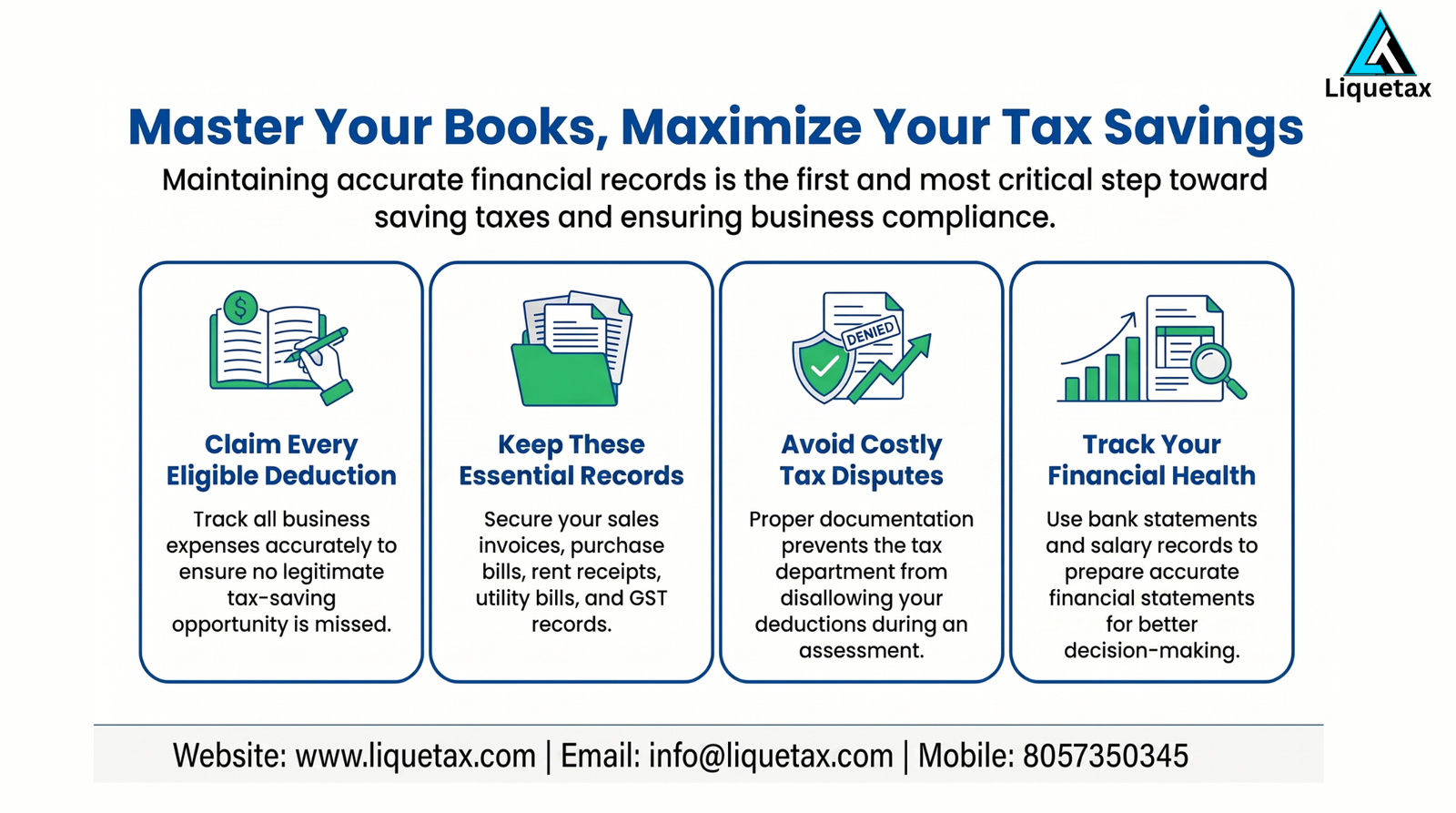

1. Maintain Proper Books of Accounts

The first step toward tax savings is maintaining accurate financial records. Proper bookkeeping helps you: Track business expenses Claim all eligible deductions Avoid tax disputes Prepare accurate financial statements Keep records of: Sales invoices Purchase bills Rent receipts Utility bills Employee salaries Bank statements GST records Without proper documentation, many legitimate deductions may be disallowed during assessment.

2. Claim All Business Expenses

One of the most effective ways to reduce taxable income is by claiming genuine business expenses.

Common Deductible Business Expenses

Office Rent

If you operate from a rented office, shop, warehouse, or commercial space, rent paid can be claimed as a business expense.

Electricity and Internet Bills

Business-related electricity, internet, and phone expenses are deductible.

Employee Salaries

Salaries, wages, bonuses, and staff benefits are allowable deductions.

Professional Fees

Payments made to: Chartered Accountants Lawyers Consultants Tax Advisors can be claimed as expenses.

Business Travel

Travel expenses incurred for business purposes are deductible.

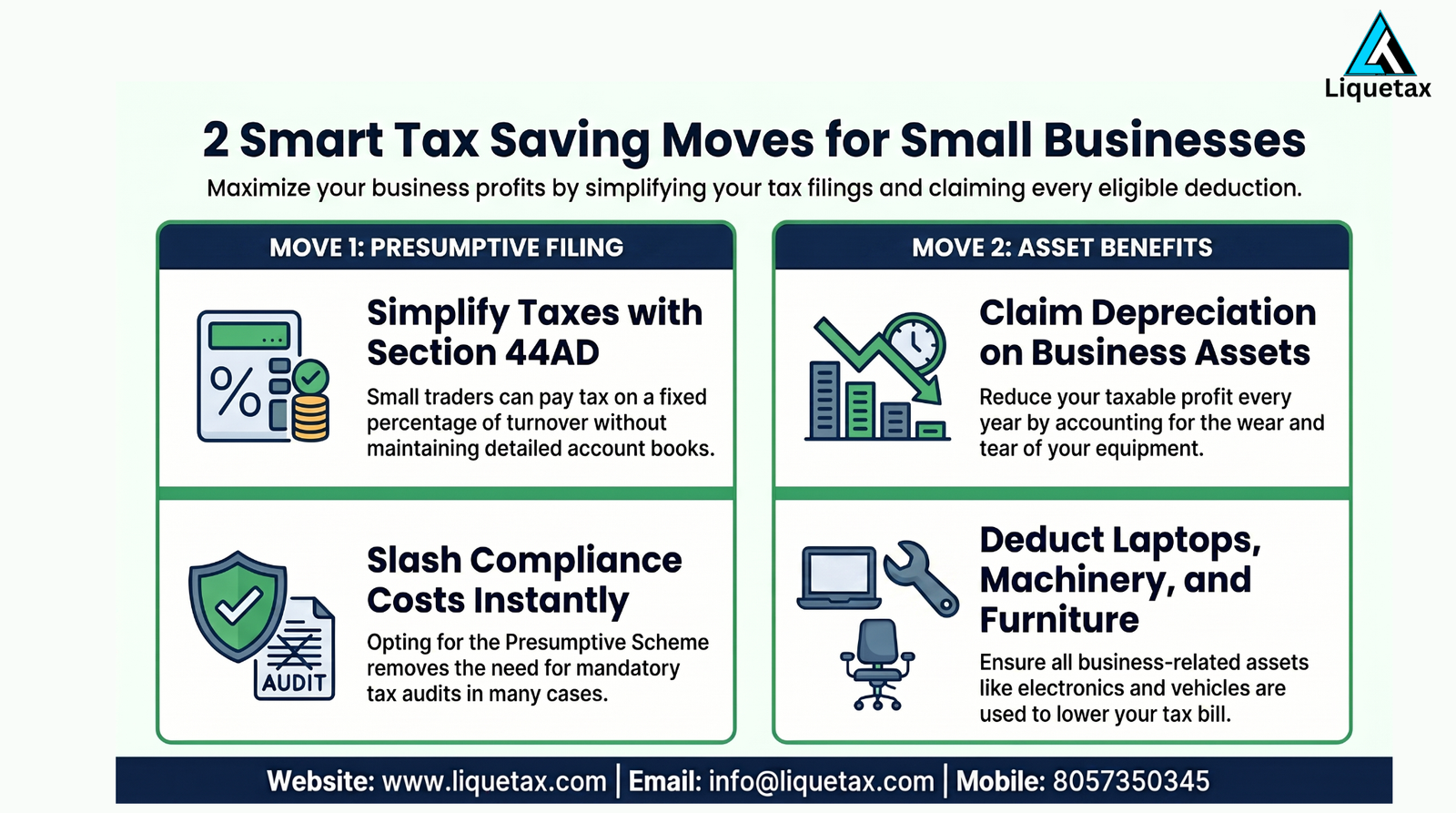

3. Use Presumptive Taxation Scheme

Small traders and businesses can benefit from the Presumptive Taxation Scheme under Section 44AD.

Who Can Use Section 44AD?

Businesses with turnover up to the prescribed limit under the Income Tax Act can opt for this scheme.

Benefits

No need for detailed books of accounts No mandatory tax audit in many cases Simplified tax filing Lower compliance burden Under this scheme, a fixed percentage of turnover is treated as profit. This can significantly reduce compliance costs for small businesses.

4. Claim Depreciation on Business Assets

Businesses can claim depreciation on assets used for business purposes. Eligible Assets Computers Laptops Printers Machinery Furniture Vehicles Equipment Depreciation reduces taxable profits every year. Many businesses fail to claim depreciation properly and end up paying higher taxes.

5. Deduct Interest on Business Loans

If you have taken a loan for business purposes, the interest paid can be claimed as a deduction. Examples Working capital loans Machinery loans Business expansion loans Overdraft facilities Interest expenses can substantially reduce taxable income.

7. Separate Personal and Business Expenses

One of the most common mistakes among small businesses is mixing personal and business transactions. Maintain: Separate business bank account Separate business credit card Separate accounting records This improves transparency and ensures only genuine business expenses are claimed.

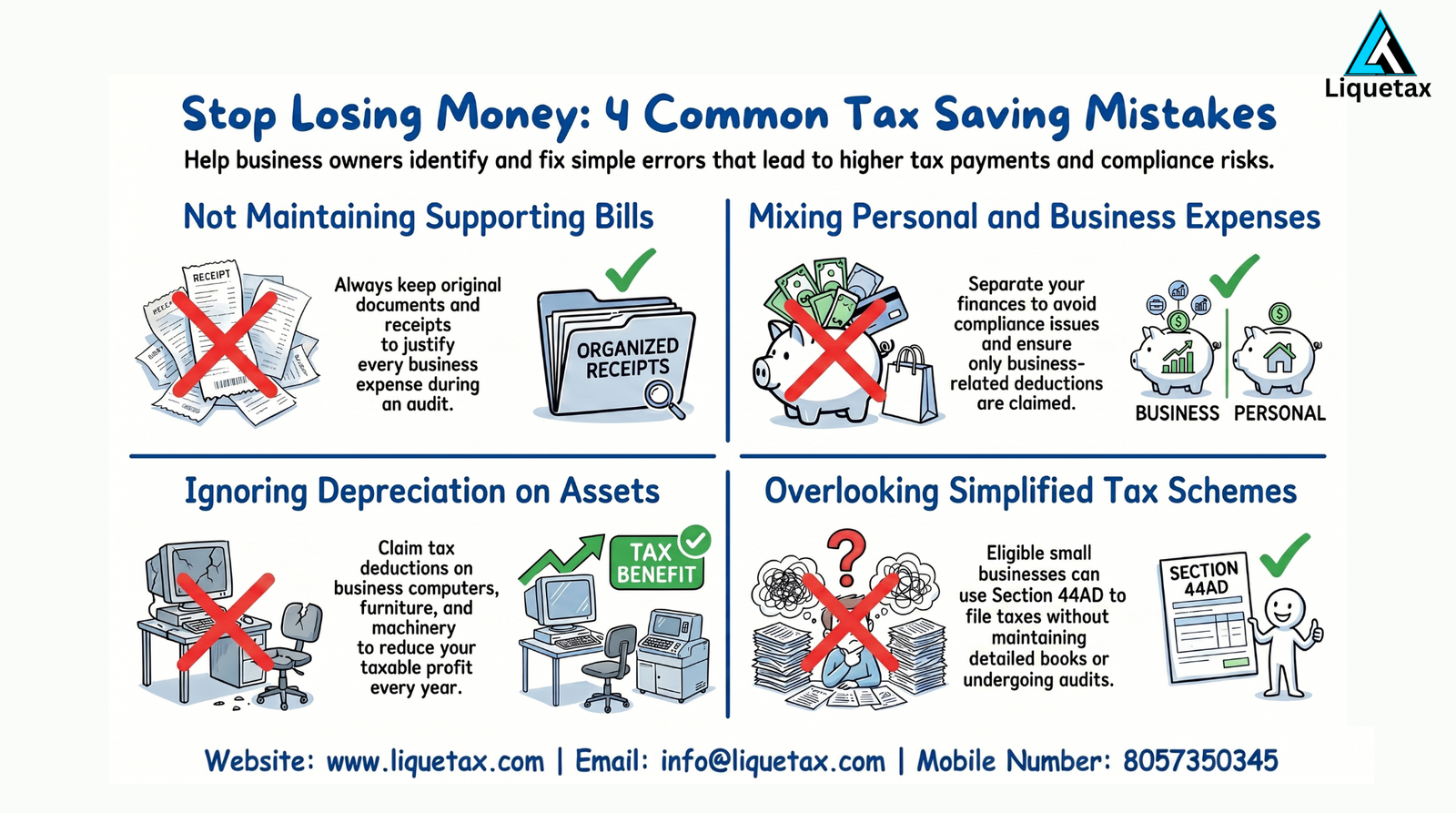

Common Tax Saving Mistakes to Avoid

Not Maintaining Bills

Always keep supporting documents for expenses.

Mixing Personal and Business Expenses

This can create compliance issues.

Ignoring Depreciation

Many businesses miss out on valuable deductions.

Late Return Filing

Late filing may lead to penalties and loss of benefits.

Incorrect GST Compliance

Errors in GST returns can become costly.

Tax Planning Checklist for FY 2026-27

✔ Maintain proper books of accounts ✔ Claim all eligible business expenses ✔ Consider presumptive taxation if eligible ✔ Claim depreciation on assets ✔ Deduct business loan interest ✔ Invest in tax-saving instruments ✔ Keep business and personal finances separate ✔ File GST returns correctly ✔ Pay advance tax on time ✔ Consult a tax professional regularly

Conclusion

Reducing taxes legally is not difficult when proper planning is done throughout the financial year. Traders and small business owners can significantly lower their tax burden by maintaining records, claiming eligible deductions, using presumptive taxation where applicable, and following proper compliance procedures. The key is to start tax planning early instead of waiting until the return filing deadline. Small efforts throughout the year can result in substantial tax savings and improved profitability. A professional tax review can help identify additional opportunities specific to your business and ensure full compliance with Indian tax laws.

Frequently Asked Questions (FAQs)

1. How can small businesses reduce tax legally?

Small businesses can reduce tax by claiming business expenses, depreciation, loan interest, tax-saving investments, and using eligible presumptive taxation schemes.

2. What is the best tax-saving option for traders?

Maintaining proper accounts, claiming all business expenses, and opting for presumptive taxation where eligible are among the best tax-saving options.

3. Can business loan interest be claimed as a deduction?

Yes. Interest paid on business loans is generally allowed as a business expense.

4. Is GST registration compulsory for all traders?

GST registration depends on turnover limits and the nature of business activities.

5. What happens if I do not maintain business records?

You may lose valid deductions and face difficulties during tax assessments.